Continuing the beverage boom

Image: Hell Energy

Evert van de Weg studies the growth pattern of the beverage can market with Mark Smyth, author of the recent Smithers study The Future of Metal Packaging and Coatings to 2027.

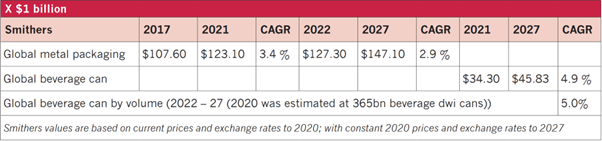

The global metal packaging market is burgeoning, with beverage cans playing a huge part in its growth. According to a report from industry insights expert Smithers, the global beverage can market is expected to see an annual growth rate of 4.9 per cent from 2021-2027.

Mark Smyth, author of this Smithers report and expert in the beverage can and metal packaging fields, outlined for CanTech International the many factors involved in the market’s staggering trajectory.

“The beverage can market was already growing at an increased rate pre-pandemic. The pandemic accelerated this growth which is now about five per cent per annum globally and we estimate it is set to remain through to 2027. When we look at the market we include investment commitments, as well as consumption, trade statistics and annual reports, so we have a forward view, not just a rearview mirror when making estimates. The beverage can growth is in the main markets of carbonates, beer and energy drinks, plus more new products in the ‘other beverage cans’ category like seltzers, coffee etc.”

Canned water is also just starting to take off, according to Mark, who mentions that brands such Evian (Danone) and Dasani (Coca-Cola) are now introducing cans as well as their bottled water offering. Nestlé Perrier is also expanding its water range to include packaging in cans.

When asked if he thinks brand owners and retailers are fully aware of beverage cans’ sustainability credentials compared to PET bottles for example, Mark responds, “This is where we run into politics and arguments; we should ask ourselves what is the truth? The truth is that metal has and always will have value. Plastic has always had a waste issue but is improving its recyclability.

The canned water segement is seeing some gradual expansion. Image: Polina Tankilevitch / Pexels

“To a packaging converter in the USA and Europe, metal (aluminium and steel) paper and glass all have a positive recycling value which more than outweighs the cost of recycling, but plastic has a negative value. Metal packaging is in a great position so we all have to push to become better and continue to maintain the package share.”

But what about cost? “It is not that difficult to make total cost of ownership using cost – leave price and margins out. Many companies have this. What it shows us is strengths and weaknesses when comparing several supply chains, all the way along the chain to the point of use, even re-use.

“While plastic has a very low cost at the point of sourcing for filling, from then on in many chains it attracts more cost than other packaging. Filling speeds are higher with metal, costs in replenishing cans in store may be lower, and additionally, the service life of the metal package is much longer and that has a value. We start to see this in the Extended Producer Responsibility tariffs rolling out across Europe where, in all the tariffs I have seen, metal has a lower tax compared to plastic.”

So what could the aluminium industry and can makers do to make more people aware of metal packaging’s benefits? “In my view we should have a road map about what each company is doing and what its respective industry is doing about the UN sustainable development goals, the packaging waste legislation and carbon neutral 2050 target. The consumer is fed up with being provided information on packaging only to often find it is incorrect. It is only recently that consumers have started to ask why not use metal, or why not refill a metal or glass container? Consumers will in the end decide on the preferred package, and have said in several studies they will pay more for sustainable packaging.”

Legislation also has its role in the battle between packaging formats. On this subject, Mark comments, “Legislation may predicate a type of packaging, but it can lead to unintended consequences, so we should be careful and ensure our businesses are well prepared and can lobby legislators and, in this way, protect the overall share for the country or region. We estimate that the overall share for metal packaging will be worth 13 per cent worldwide in 2022. The consumer ultimately has the purchasing power, however. In the noughties we have seen the power of social media leading to changes in demand. Engaging with and satisfying the consumer is key.”

When asked whether the availability of the right aluminium grades for the production of beverage cans is a limiting factor, Mark responded that “aluminium for beverage cans will always compete with other markets for aluminium. With 5000 series the competition is with automobiles. The history of aluminium expansion has been favourable, there is no reason to doubt that investments will be made as required, which is what we see for instance in Alabama USA and the new hot rolling in Greece.”

Are aluminium producers doing enough to enable the use of recycled aluminium? “Recycling aluminium saves 95 per cent of the energy that would otherwise be used to produce aluminium. What that means today for a converter is at least a €1.7 per kilo value for scrap. Compare that to a converter having to pay €0.20 to €0.40 per kilo more for recycled PP or PET material. There is a fundamental incentive to recycle aluminium. The recycling we have, which is over 76 per cent in 2019 in Europe and increasing, is part of the reason why aluminium packaging is so successful.”

Engaging with and satisfying the consumer is key. Image: Andrea Piacquadio / Pexels

Regarding the beverage can stock market, Mark says, “When we look at the stock markets, there is the financial performance and then there is the feeling or sentiment, the two are multiplied to arrive at the value. There are many ways of trying to model this, and it is always going to be complicated. What really matters is your performance or last sale versus budget and in that respect, the beverage can is performing very well. In any market, whenever there is growth, then the sentiment or feeling improves. Looking at the beverage can, the time is now: growth has increased from just over three per cent historically to five per cent worldwide.

“On the other hand, the investments are significant and as with everything there are risks which are right at the front of every quoted company’s annual report, so be careful in drawing conclusions. How will the topics we just discussed impact the forecast? What does the war in the Ukraine mean? Russia is the world’s largest aluminium producer after China and is a leader in decarbonisation; there is going to be a shortage in primary aluminium, but hopefully for just a short period. There are other markets in the can business, apart from beverage can, which can be equally interesting. Just look at the changes in food can supply, for instance the formation of Eviosys and the takeover of Ball Metalpack by Sonoco in 2021. Now in 2022 we have the global food and specialty can manufacturer Trivium in a sale process, so there are always opportunities and they are not exclusive to beverage cans.”

So, will there be a shortage of beverage cans in the future, in order to keep up with demand? Mark concludes, “The shortage of beverage cans manifests itself in the USA, the world’s largest market, as empty can imports. We can follow the empty can imports through trade statistics, and see they were over 12 billion last year into the USA. In 2022 they are still there at a much lower level as new plants come on stream. Since it costs almost the same again to import as buy in the local market, as capacity comes on stream the imports will disappear probably by 2023. Elsewhere the market is tight, with capacity being added in every region, including the world’s smallest region, Australasia.”

For the full Smithers report, visit www.smithers.com/en-gb/services/market-reports/packaging/the-future-of-metal-packaging-and-coatingsto-2027. CanTech International readers are able to use the discount code MP27CAN until the end of August.

- Mark Smyth founded MS Can Solutions in 2019, providing business, marketing, and packaging intelligence to the packaging industry. He also has experience working for American Can, NaCanco, American National Can, Pechiney, Impress and Ardagh Group.

Topics

aluminium industry beverage cans recycling

PeopleOrganisationsBall Metalpack coca cola Danone Dasani Evian Nestlé Perrier Trivium

Regions