EPR – who’s calling the shots?

Time is running out to ensure fair and informed regulation, says MPMA’s Jason Galley

Jason Galley became the Metal Packaging Manufacturers Association’s director and chief executive at the start of the year, and his first major challenge is ensuring that EPR delivers a fair and accurate assessment of metal as implementation in the UK looms. Here, Galley looks at what the next stage holds.

Jason Galley became the Metal Packaging Manufacturers Association’s director and chief executive at the start of the year, and his first major challenge is ensuring that EPR delivers a fair and accurate assessment of metal as implementation in the UK looms. Here, Galley looks at what the next stage holds.

Extended Producer Responsibility – EPR – has been a long time in development, or so it seems, and now it’s been delayed further to October 2025. This is both good and bad news.

Bad for the companies that need to plan and budget for their modulated fee obligations; they don’t currently know what these will be, but in other respects good for metal, because there’s still time to influence outcomes further.

To some, this situation will seem disappointingly familiar. Turn the clock back some ten years; the Courtauld Commitment at that time initially cited that a material’s sustainability credentials should be measured by its weight to landfill. This proposal would have clearly disadvantaged metal, despite it having the highest recycling rate of any material. Then, as now, clear presentation of metal’s ‘permanently available’ status was key to getting this changed.

‘Metal Recycles Forever’ was introduced and has become our sector’s watchword, along with the presentation of metal’s second-to-none recycling infrastructure, and its ease of collection for recycling. Collectively, these placed metal among the highest recycling rates of any packaging material.

Fast forward ten years and we now find ourselves in a similar position with EPR.

EPR positions responsibility for the end-of-life management of a product with the producer or local authority. So far so good, because this will give producers a direct incentive to ensure they use materials with high recycling rates: the higher the recycling rate, the less they pay in modulated fees.

In turn, so the thinking goes, producers will invest in new and expanded material collection systems, recycling infrastructures, and engage in public awareness programmes that encourage recycling. The recycling rate will rise.

Who’s responsible?

Measurement criteria for this has, however, been outsourced by government to consultancy, and an assessment model has been developed. Top of the list is ‘Highly Recyclable Materials’ which, as its name suggests, encompasses materials that have well-established recycling markets and infrastructure. But there is a conspicuous weakness inherent in this classification – its abject failure to differentiate between different multiples of recycling.

How can products and materials that can be recycled just once into something that itself is unrecyclable, in a purely linear process, be classified in the same category as others that can be recycled a few more times? And these in turn to products and materials that are fully circular and can be recycled again and again, for example a ‘permanently available’ material such as metal?

This current thinking suggests that when a product’s material is recycled, that’s it. Job done.

But the truth of the matter is that only those materials that can be recycled over and over again, with no loss of quality – permanently available materials – truly contribute to a fully circular economy. Anything else is not circular, and therefore not sustainable.

It is of grave concern that the very people imposing these measures often simply don’t get this – whether in government or outside.

Why the confusion?

Part of this ignorance, for want of a better word, is down to the revolving door of government ministers, civil servants and indeed consultants who come and go with alarming regularity, taking with them a wealth of knowledge and often months, years even, of work by organisations like MPMA to help shape policy from a well-informed base. This is important, because where whole sectors are impacted by decision making, consistency matters.

So, for EPR, if a product’s evaluation main criterion is its recyclability, you really need to understand the difference between a permanently available material that can be recycled any number of times, and one which has a much more limited life.

Any recyclability assessment should surely value those materials that be recycled repeatedly, more than those that cannot.

It’s great that the concept of high-quality recycling is captured in PPWR – but it doesn’t go far enough. We should really recognise and reward the environmental value of those materials that can be recycled over and over without loss of their intrinsic properties.

Modulated fees are dependent on recyclability and recycling rates and, if done well, this all makes sense. But these fees will undoubtedly add to the price of the product, so consumers should know that the additional costs they will have to bear are genuinely contributing to improved recycling rates. If they don’t, we will see only market distortions and not the environmental benefits that are sought.

The reality is that there could easily be double-digit pence-per-unit cost swings – significant amounts that will impact purchasing decisions. This might be acceptable if it leads to a circular economy, but a tragedy if it doesn’t.

Funding for local authorities is not tied to any meaningful performance and there is no incentive to drive for success or inclination to outshine government. There seems to be nothing that will hold local authorities to account.

So, it is clear that industry should be in charge, and we are pleased that DEFRA and its agencies

are consulting. MPMA will be in the room and in a position to provide the advocacy, education and arguments that ensure DEFRA officials at least know of these assets.

Rocks in the road ahead

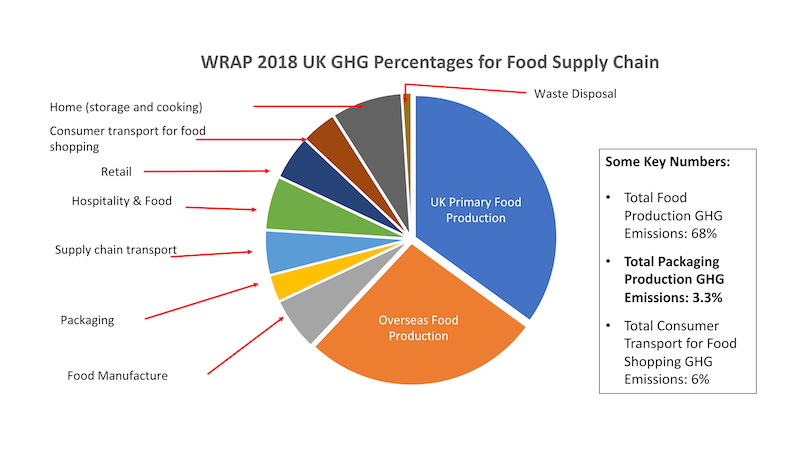

Graph: WRAP

A broader issue with EPR, and one which is not just about metal, is mission creep. EPR could be extended to include carbon capture, refill, and perhaps other environmental criteria such as reuse. This would introduce a whole new set of criteria – and all fairly arbitrary.

Take carbon. A WRAP study showed that two thirds of GHGs in the UK food chain emanate from food production. Just three per cent was attributed to packaging and, to give further context, six per cent was in consumer transport.

Packaging protects the carbon spent in producing food: it is part of the solution and of course it can be further decarbonised – but we must be careful. UN data says that we waste a third of food globally, so this is clearly where the big decarbonising actions should be – especially as the population grows and land use changes due to a burgeoning population or climate change. And, as we all know, nothing can compete with the shelf life, and therefore waste minimisation, of a food can!

Where we must be especially careful is in defining the problems to be solved before prescribing the solution. This is why the full involvement of industry is so important. It has a critical role in helping define a problem, with all affected parties able to make their case. It is industry that knows how to find solutions to these problems and in this respect has an excellent track record. Government clearly must be an arbiter, but experience suggests that it can also stifle rather than engage.

I still see materials selection books developed for brands and retailers that give one figure for the sustainability of a material based on its weight. This disregards any value of innovation towards decarbonisation – for example hydro-powered aluminium smelting – and even take-back schemes to increase recycling rates.

In fact, there are NGOs looking right now at schemes which go beyond what government is doing on EPR which, while well meaning, can be ill informed and potentially problematic to progress.

Another fear is that EPR becomes a gravy train for local authorities. Currently, to receive funding from EPR fees, local authorities will only have to hit 80 per cent recycling rates. But this is far from what is achievable and brings the 80/20 Pareto Principle to mind – in this case the final 20 per cent requiring disproportionately greater effort and expense. Where is the incentive to do better than 80 per cent? Beverage cans, for example, are already at 82 per cent, and this will certainly rise when DRS comes in and consumers are incentivised to return their cans for recycling.

The UK is almost unique in going for a government controlled EPR, rather than one that is controlled by obligated parties. So, the very least it can do is ensure that all obligated parties have a good share of voice.

MPMA’s task ahead is to continue to ensure that its voice is heard and make the case for a fair and genuinely circular EPR assessment.

Topics

Extended Producer Responsibility (EPR)

PeopleOrganisationsMetal Packaging Manufacturers Association (MPMA)

Regions